Blog, Technology

April 3, 2026

AI-Powered Commercial Banking Solutions: 5 High-Impact Use Cases for Relationship-Driven Growth

How data-driven insights and artificial intelligence (AI) can strengthen commercial relationships by...

October 2023 marked the end of a more than three-year pause on federally-backed student loan payments, and millions of Americans are now navigating a new financial landscape. This resumption, amidst record-high inflation impacting essential costs like housing and food, is placing considerable strain on borrowers.

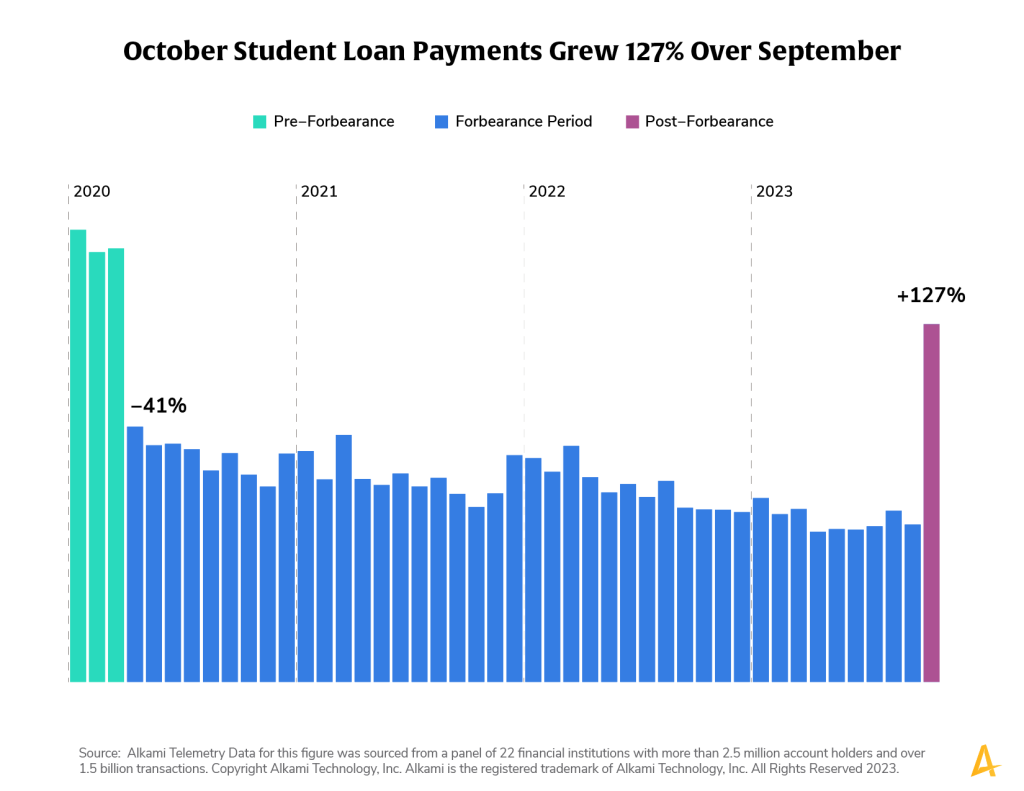

Data from Alkami Technology shows a 127% increase in student loan payments in October compared to the previous month. This surge indicates a significant financial shift for account holders, who now face the additional burden of student loan expenses after a prolonged period of economic challenges.

However, nearly 9 million borrowers “missed their first student loan payment…meaning 40% of the 22 million borrowers who had payments due in October, did not make payments by mid-November” according to cnn.com.

Actions financial institutions can take…

Leverage first-party transaction data to observe those who have new or increased monthly student loan expenses. After more than 18 months of rising economic prices, these payments could be a very stressful addition to their personal finances. It’s also useful to watch for who may be missing payments, as an indicator of further economic stress.

Financial institutions must recognize the challenges faced by account holders. Rising economic pressures combined with the resumption of student loan payments could lead to heightened financial stress. It’s crucial for banks and credit unions to stay informed about their account holders’ new monthly expenses and provide support during this transition.

Knowing who is struggling is just half the battle. It is also vital that banks and credit unions demonstrate that they understand the struggles some may be going through. Just as you would not market a new home loan to someone who already has a mortgage with your institution, data can inform a financial institution to market relevant products to those account holders who need them the most to support their financial journey.

Borrowers do have different repayment options, like income-driven repayment (IDR) plans, to better manage their finances. For borrowers struggling with payments, IDR plans can offer relief based on income and family size, with the new SAVE Plan being a particularly affordable option.

The Department of Education has instituted a 12-month “on ramp” for borrowers, which runs until September, 2024. It means that, during this period, if borrowers miss monthly payments, they will not take a hit on their credit, the loans will not be reported to credit bureaus as delinquent nor will they be referred to debt collection agencies. This measure is critical, as past economic downturns have shown that borrowers entering repayment during such times default more quickly than those in more stable periods.

How can a financial institution support account holders, even though they are not their loan provider?

The above analysis looked at the impact these resumed payments had on borrowers who had federally-backed loans that were suspended during the pandemic. But that doesn’t tell the whole story. They aren’t the only cohort affected by student loan debt.

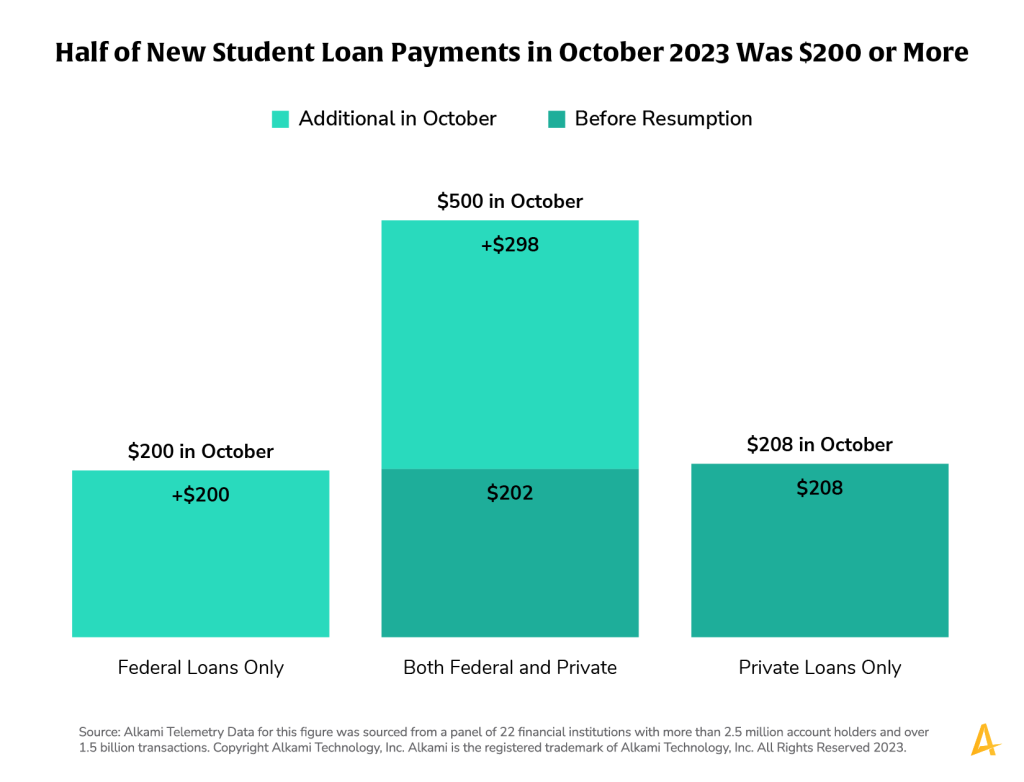

Some student loan borrowers had a mix of federally-backed and private loans. Only the federally-backed loans were suspended; borrowers kept on paying their private loans throughout that period. The analysis showed that this group had a median payment of $202 for the private loans they continued to repay during the pandemic, and the resumption of the federally-backed loan added $298 to that.

Then, there is a group who only had private loans. They did not benefit from the forbearance and continued to make their payments throughout that period, a median of $208, which, depending on the size of their loan, they are still repaying.

For some, that new expense might not be a significant burden, especially if they don’t have much in the way of other debt. But for others, it could have quite a significant impact, because the new loan payment does not exist in a vacuum. These account holders have other monthly expenses, like credit card payments, mortgages, car loans and more.

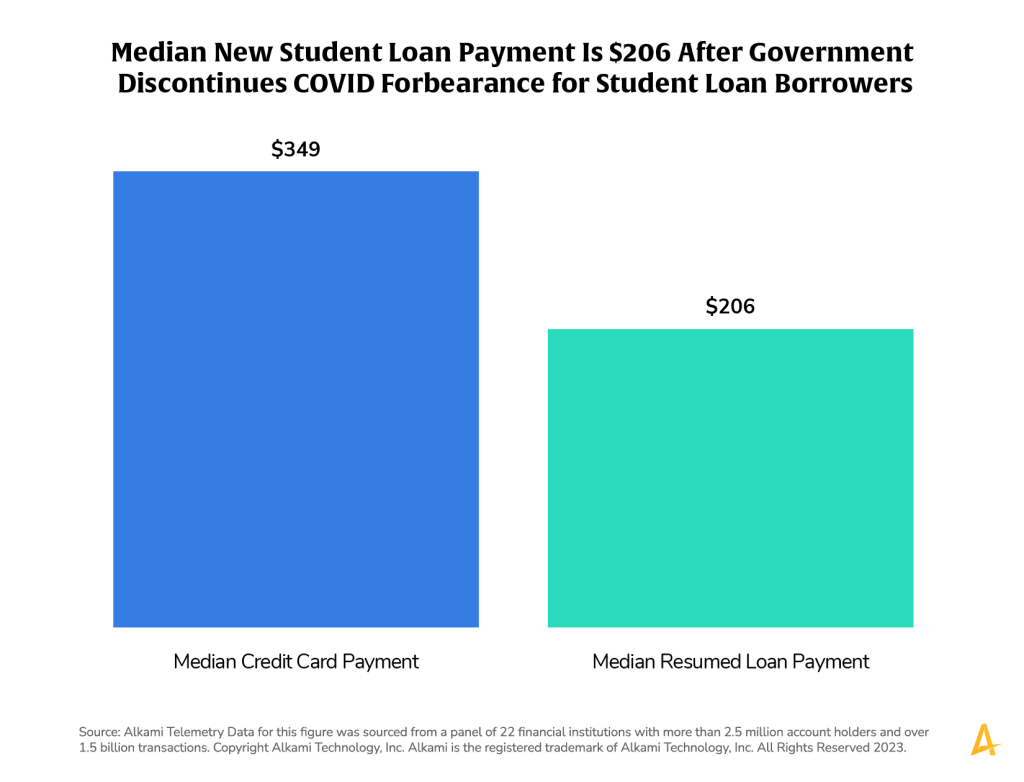

Contextualizing the burden of that new $200-300 with a broader understanding of the other monthly payments that borrower already has, can give a clear picture of the new payment’s true impact on each borrower. As a benchmark, Alkami compared the median resumed payment to the credit card payments for this same group and found that their loan payment represented roughly 60% of their credit card payment amount.

Key takeaway…

The extra monthly expense that many student loan borrowers incurred in October could pose a significant burden on their budget, straining their finances. Financial institutions need to know which of their account holders are feeling the stress of these new payments and respond with advice, education and offers that will impact people in the right ways at the right time. Might a lower-interest home equity loan to consolidate high interest debt be a solution?

As the American banking industry faces the challenge of deposit growth amidst changing economic conditions, understanding and responding to the dynamics of student loan repayments becomes crucial. Financial institutions have a pivotal role in guiding their account holders through these changes and ensuring that the systems in place are ready to support those facing difficulties.

Source: Alkami Telemetry Data for this figure was sourced from a panel of 22 financial institutions with more than 2.5 million account holders and over 1.5 billion transactions.