Blog, Strategies

July 24, 2026

How Standardized Credit Attributes Drive Smarter Lending

Automated data normalization empowers underwriting teams to make faster, more consistent credit deci...

Over the next ten years, the United States will experience an immense transfer of wealth from older Americans to largely Millennials, Generation Z (Gen Z), and Generation X (Gen X). $16 trillion to be exact.

Wouldn’t you want your financial institution to retain or acquire a piece of that pie?

These consumers are about to inherit the greatest transfer of intergenerational wealth, which is a huge opportunity for financial institutions to capture deposits and establish life-long relationships.

But winning trust and loyalty comes with diligence and commitment to meet the expectations of these generations.

According to Alkami’s primary research, 48% of Gen Zs and Millennials have had such a bad digital experience with a financial provider that they opened a new account with another.

Meaning if account holders are dissatisfied with your consumer banking solutions, they will look elsewhere, most likely without closing their existing account – opening the door to silent attrition.

Many consumers leverage a multitude of financial relationships to manage their finances. They turn to different providers to deposit their paycheck, manage their budget, check their credit score, invest, make person-to-person (P2P) transfers, monitor their home value, purchase via buy now pay later, and more.

With each provider offering a niche solution, consumers have grown accustomed to a network of providers.

However, each of these disparate relationships is targeting your hard-earned account holder with enticing competitive offers. Rather than letting millennials and Gen Z leave your institution, financial institutions must deploy a strategy to prevent “ghosting.”

To inform retention efforts, The Financial Brand recommends that banks and credit unions:

To keep consumers engaged and win the primary banking relationship, financial institutions must deliver intuitive consumer banking solutions that bring all of the digital banking tools they need under one roof.

Financial institutions should reimagine how they have traditionally viewed their digital banking platform.

Instead of using digital as simply a self-service channel, banks and credit unions should leverage their digital banking solutions to drive strategic business objectives – creating back-office efficiency, generating new revenue opportunities, accelerating acquisition efforts, lowering costs and innovating at scale.

By introducing a digital sales and service platform, financial institutions can stay ahead of consumer expectations and needs and deliver a best-in-class user experience with personalization at scale.

48% of Gen Z use social media for investment advice, however, they also prefer face-to-face communications whether it’s in-person or virtual assistance. Meanwhile, millennials, “have embraced digital-only banking and digital wallets more than any other generation.”

Taking those observations into consideration, there are many opportunities where financial institutions can strengthen banking relationships, build loyalty, and accelerate engagement. Financial institutions should rethink how they traditionally have marketed to these audiences.

For instance, a Gen Z customer or member may respond better to a local influencer they trust promoting a certificate of deposit (CD) rate with your institution, compared to email marketing.

However, it’s not only about how you market to these account holders during the acquisition process, but how you engage with them throughout the banking journey to power retention efforts.

Gen Z consumers are digital natives and are the first generation to grow up never knowing the world without the internet.

Can you imagine that?

They expect convenience and speed in transactions, including financial ones. Gen Z has quickly adapted to and is comfortable with digital payment options. As a generation that was born between 1996 and 2010, they came into their adulthood amid the COVID-19 pandemic and were negatively affected financially as a result.

But it wasn’t just Gen Z who felt their adulthood and career journeys were put on pause. According to Forbes, “32% of millennials and Gen Zers moved back home with their parents during the pandemic…more than half of those who moved home say it was out of necessity.”

These account holders need support to get back on their feet and build a successful future for themselves. However, these consumers have strong expectations from their banking relationships. How can financial institutions cater their banking services to grow relationships with Gen Z? Here’s where bank and credit union marketers can activate their skills.

Per Alkami’s eBook, How Banks and Credit Unions Can Attract and Retain Gen Z, these financially powerful account holders can be retained by putting the following tactics into action:

1. Highlighting Social Responsibility and Inclusivity Efforts

A Harris Poll commissioned by Google Cloud found that 82% of shoppers want to patronize companies with values that align with their own. And 75% said they had parted ways with a brand over a conflict in values. Social responsibility can mean a lot of different things. Odds are many financial institutions currently support a cause that fits within this spectrum. This is a great opportunity for financial institutions to talk about their commitments to supporting local businesses and communities, environmental causes, charities, diversity, equity & inclusion, etc.

2. Delivering Market-Leading Consumer Banking Solutions

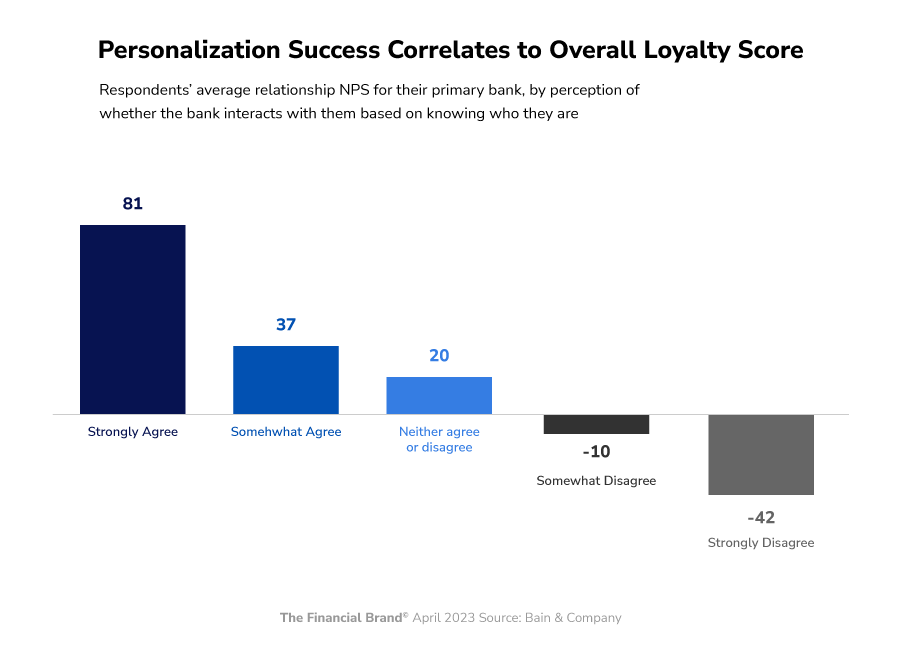

A better digital banking experience translates into a better user experience, which in turn translates to greater loyalty and engagement. Similar to their day-to-day digital interactions, consumers want personalized banking.

Not only do they expect individualization across their digital banking platform, but they also expect all of the innovative fintech solutions that are marketed directly to them within the banking experience.

Rather than having your digital banking users turn to third-party apps, financial institutions can deliver modern in-app solutions. This is where a strategic partner ecosystem can enable financial institutions to quickly deploy market-leading fintech solutions without burdening staff with development efforts.

While Gen Z cares about convenience, they’re also very concerned about security. Two recent surveys from PYMNTS.com and Digital Information World indicated that privacy for Gen Z was more important to them than metrics such as speed.

They’re fully aware of the inherent risks of digitization and want to ensure their data and dollars are protected. It’s paramount that financial institutions take a proactive security approach by alerting account holders to potential threats and using transaction data to flag accounts with suspicious activity.

3. Creating a Sense of Belonging for Gen Z Account Holders

All generations of account holders want a best-in-class user experience. What makes Gen Z unique is that they want to feel known by the financial institution they choose to bank with. So how can banks and credit unions better understand their customers or members?

By activating transaction data cleansing and uncovering actionable insights about account holders. Think about transaction enrichment as a goldmine when marketing for financial institutions.

By pairing account holder insights and marketing automation with a digital banking platform, financial institutions can deliver the right message to the right user at the right time.

Financial institution marketers can target Gen Z account holders with personalized engagements and drive cross-sell efforts with hyper-targeted offers.

It’s time to transform your digital banking platform into a powerful sales and service engine that drives revenue for your institution and strengthens relationships with younger demographics.

Discover how Alkami’s retail banking solutions can help your institution exceed your account holders’ expectations for a modern digital banking experience.